Post-Service Insurance

An Explanation of Benefits (EOB) is not a bill, though it is frequently mistaken for one. It is a communication from your insurer—whether that is UnitedHealthcare, Aetna, or Blue Cross Blue Shield—detailing how a recent medical claim was processed. It acts as a bridge between the provider's high "sticker price" and the negotiated rate your insurance actually pays.

Consider a standard MRI scan. The hospital might list the price at $3,500. However, through your insurer’s PPO or HMO network, the "Allowed Amount" might only be $800. The EOB shows you this discrepancy, ensuring you aren't charged the remaining $2,700, which is often referred to as a "contractual write-off." Without reviewing this document, you might blindly pay a provider's invoice that hasn't yet accounted for insurance adjustments.

Statistics suggest that medical billing errors are more common than most realize. According to the Medical Billing Advocates of America, nearly 80% of medical bills contain at least one error. These errors often range from "unbundling" (charging separately for procedures that should be a single charge) to simple clerical mistakes that can cost patients hundreds of dollars in unnecessary out-of-pocket expenses.

Ignoring Your Paperwork

The primary danger of neglecting your insurance statements is financial "double-dipping." Many patients pay the "estimated" amount at the doctor’s office, only to receive a bill later that doesn't reflect the insurance company's final decision. If you ignore the EOB, you lose your only tool for verifying that the doctor's bill is legitimate and matches the insurance company’s determination of your responsibility.

Furthermore, failing to spot a "Denied" status on a statement can lead to medical debt being sent to collections. Sometimes a claim is denied simply because a provider used the wrong ICD-10 diagnosis code or failed to include a required NPI (National Provider Identifier) number. If you don't catch this on the EOB, the provider may eventually turn the balance over to a collection agency, impacting your FICO score and overall financial health.

Real-world scenarios often involve "balance billing," where an out-of-network provider attempts to charge the patient the difference between their high rate and the insurer's payment. Since the No Surprises Act took effect in 2022, many of these practices are illegal for emergency services, but the EOB remains your first line of defense in identifying when these protections should be triggered.

Managing Medical Claims

Verify Provider and Service Accuracy

Check the date of service and the name of the physician. It is not uncommon for a billing department to accidentally swap digits in a member ID, resulting in a claim being processed under the wrong plan or denied entirely. If you see a service listed that you didn't receive, it could be a sign of "upcoding," where a provider bills for a more complex (and expensive) version of the service actually rendered.

Decode the Remark Codes and Denial Reasons

Every statement includes a "Reason Code" or "Remark Code" section. These are alphanumeric tags like "CO-45" or "PR-1." Do not ignore these. They explain exactly why a portion of the claim wasn't paid. For example, a code might indicate that the service requires "prior authorization." If you see this, you can call your doctor’s office to have them retroactively submit the paperwork, potentially saving you thousands of dollars.

Track Your Deductible and Out-of-Pocket Progress

Your statement typically shows a running tally of your annual deductible. Apps like HSA Bank or Betterment can help you manage the funds, but the EOB is the official source of truth. If you have a $3,000 deductible and you’ve met $2,800, your next $500 visit should only cost you $200 before your co-insurance kicks in. Monitoring this ensures you aren't overcharged during the "transition" phase of your plan year.

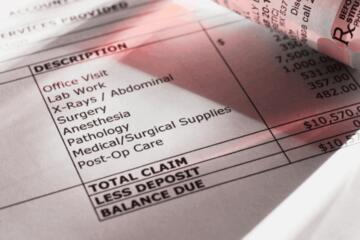

Match Statements with Provider Invoices

Never pay a doctor's bill until you have the corresponding insurance statement in hand. Use tools like Quicken Simplifi or a simple spreadsheet to line up the "Patient Responsibility" amount on the statement with the "Amount Due" on the doctor's invoice. If the numbers don't match exactly, do not pay. Call the billing office and ask why their records differ from the insurance company's determination.

Utilize Digital Transparency Tools

Modern insurers provide digital portals and mobile apps (like the MyCigna app) that offer "Price Transparency" tools. Before a procedure, use these to estimate your cost. After the procedure, compare the actual EOB to your estimate. If there is a massive variance, you have the evidence needed to negotiate or appeal the claim. This proactive approach turns a passive document into a financial negotiation tool.

Review the No Surprises Act Protections

If you receive care at an in-network facility but are treated by an out-of-network specialist (like a radiologist or anesthesiologist), the EOB should reflect that you are only responsible for in-network cost-sharing. If the statement shows you owe out-of-network rates for an emergency, you must flag this. The CMS.gov (Centers for Medicare & Medicaid Services) website provides a portal to report these specific violations if your insurer fails to correct them.

Financial Recovery

Case Study 1: The Miscoded Surgery

A patient at a surgical center in Chicago received a bill for $12,000 for an outpatient procedure. Upon reviewing the statement from their insurer, the patient noticed a "Remark Code" stating the claim was denied because the provider failed to submit "Clinical Notes." The patient called the provider, who realized they had missed a fax. Once the notes were sent, the claim was reprocessed, and the patient's responsibility dropped to a $250 co-pay. Total Savings: $11,750.

Case Study 2: The Double-Billed Consultation

A small business owner in Texas noticed two identical entries on their Aetna statement for a single specialist visit. The provider had accidentally submitted the claim twice under two different billing NPIs. By catching this on the statement, the patient prevented a duplicate charge from hitting their deductible, ensuring their health savings account (HSA) funds were preserved for actual future needs.

Critical Components

| Term | Definition | Wallet Impact |

|---|---|---|

| Billed Amount | The "list price" set by provider. | Usually irrelevant in-network. |

| Allowed Amount | The negotiated rate insurer pays. | Maximum provider can collect. |

| Deductible | Amount paid before insurance kicks in. | Direct out-of-pocket expense. |

| Co-insurance | Your percentage share of the cost. | Based on Allowed Amount. |

| Not Covered | Services excluded from benefits. | You pay 100% unless appealed. |

Common Pitfalls

One of the most frequent mistakes is assuming that "Denied" means the service isn't covered. Often, a denial is a "technical denial," meaning the insurer just needs more information. Instead of panicking, look for the specific code. If it says "Information Requested," call your doctor's office immediately to ensure they are communicating with the insurance company.

Another error is ignoring the "In-Network vs. Out-of-Network" status. If you see a provider you thought was in-network listed as out-of-network, check the address. Some doctors work at multiple clinics, and only specific locations may be contracted with your plan. If this happens, you can often negotiate a "Single Case Agreement" or appeal based on misleading information in the insurer's own provider directory.

Lastly, many people forget to check their "Member Discounts." Many plans provide discounts for things like lab work through Quest Diagnostics or Labcorp. If your statement shows you paid full price for a blood test, verify that the lab applied your plan's specific negotiated discount. Even a $50 difference per test adds up over a year of chronic care management.

FAQ

Why did I get an EOB if I already paid my co-pay at the office?

The co-pay is only a partial payment. The statement tracks how that co-pay was applied and whether you owe anything additional based on the complexity of the visit or additional tests performed during the appointment.

What should I do if the "Patient Responsibility" on my statement is higher than my bill?

Trust the statement from the insurance company over the bill from the doctor. Contact the doctor's billing department and point out the discrepancy. The provider is contractually obligated to follow the insurance company's "Allowed Amount" if they are in-network.

How long should I keep these documents for my records?

It is recommended to keep these for at least five years, or as long as the statute of limitations for medical debt in your state. They are also vital for tax purposes if you plan to deduct medical expenses or justify HSA withdrawals during an IRS audit.

Can I appeal a decision if the statement shows a service was not covered?

Yes. You have a legal right to an internal appeal and an external review. Use the "Appeal Rights" section usually found on the last page of the document. Success rates for appeals can be surprisingly high when supported by a letter of medical necessity from your doctor.

What is the difference between a "Facility Fee" and a "Professional Fee"?

Often you will see two statements for one surgery. One is for the hospital (Facility Fee) and one is for the surgeon (Professional Fee). You must review both to ensure you aren't being double-charged for the same specific action, such as anesthesia administration.

Author’s Insight

In my years of navigating the intersection of finance and healthcare, I have found that the Explanation of Benefits is the single most underutilized tool for consumer protection. I have personally saved over $4,000 in a single year just by cross-referencing my statements with my provider's invoices and catching simple coding errors. My advice is to create a "Medical Master File"—digitize every statement and never pay a bill the day it arrives. Patience and scrutiny are your best financial allies in the modern healthcare system.

Summary

Mastering the art of reading your insurance statements is essential for maintaining financial stability. By understanding the difference between billed and allowed amounts, identifying remark codes, and proactively matching statements with invoices, you can prevent costly billing errors and ensure you only pay what you truly owe. Stay organized, use digital tools to track your deductible, and never hesitate to challenge a denial. Taking these steps transforms you from a passive patient into an empowered healthcare consumer.