Understanding High Costs

Receiving a six-figure bill for a routine procedure is a systemic reality in the United States healthcare market. High-cost medical bills often stem from a lack of price transparency and the "chargemaster" system—a master list of prices that hospitals set, which are frequently three to four times higher than what insurance companies actually pay. For example, a single Tylenol pill might be listed at $15, while its market value is pennies.

Consider a patient undergoing an emergency appendectomy. The hospital may bill $45,000, yet the Medicare reimbursement rate for the same zip code might only be $12,000. Real-world data from the Kaiser Family Foundation (KFF) indicates that 1 in 4 adults in the U.S. have struggled to pay medical bills, with medical debt being the leading cause of personal bankruptcy in the country.

The Disparity in Negotiated Rates

Hospitals maintain different price points for the same service depending on who is paying. A self-pay patient is often charged the highest "retail" price, whereas a major insurer like Blue Cross Blue Shield negotiates a significantly lower rate. Understanding this disparity is your primary leverage when asking for a bill reduction.

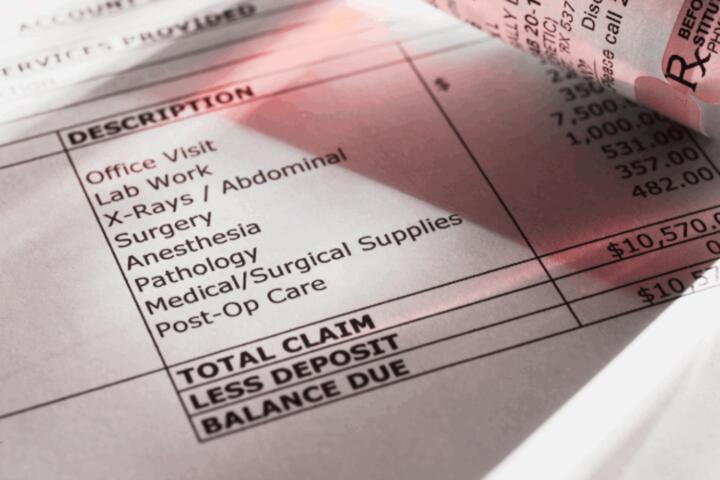

The Complexity of Billing Codes

Medical bills rely on CPT (Current Procedural Terminology) codes and ICD-10 diagnosis codes. A single digit error in these codes can change a covered preventative screening into an expensive diagnostic procedure. Expertise in reading these codes is the difference between paying full price and getting a full waiver.

Common Financial Pitfalls

The most significant mistake patients make is panic-paying or putting the entire balance on a high-interest credit card. This converts medical debt—which has some consumer protections—into consumer debt, which has none. Ignoring the bill is equally dangerous, as it leads to collections and a 100-point drop in your FICO score.

Another critical failure is accepting the first "summary" bill as the final word. A summary bill lacks the detail necessary to verify if the services charged were actually performed. Statistically, Equifax has noted that up to 80% of medical bills contain at least one error. These range from duplicate charges to "unbundling," where a single procedure is broken down into multiple smaller, more expensive parts.

Failing to verify the "No Surprises Act" protections is a common oversight. Since January 2022, federal law protects you from surprise bills for out-of-network emergency services or out-of-network providers at in-network facilities. If you receive a bill for $2,000 from an out-of-network anesthesiologist who worked on your surgery at an in-network hospital, you are likely protected by law.

Strategic Recovery Steps

The first action is to request an "Itemized Bill" with CPT codes. This forces the hospital to justify every line item. Once you have this, use online tools like Healthcare Bluebook or Fair Health Consumer to find the "fair market price" for your zip code. If the hospital charges $5,000 for an MRI and the fair market price is $1,200, you have a data-backed starting point for negotiation.

Leveraging Hospital Charity Care

Under Section 501(r) of the Affordable Care Act, non-profit hospitals are required to have Financial Assistance Policies (FAPs). These programs, often called "Charity Care," can provide 50% to 100% discounts for individuals earning up to 400% of the Federal Poverty Level. For a family of four in 2024, that could include households earning nearly $120,000 annually.

Effective Negotiation Scripts

When calling the billing office, use specific phrasing. Instead of saying "I can't pay," say: "I have reviewed the Medicare reimbursement rates for these codes, and your charges are 300% above the fair market value. I am prepared to pay the Medicare rate plus 20% today to settle the account in full." This demonstrates you are an informed consumer and provides a clear exit path for the biller.

Using Medical Bill Advocates

If the bill exceeds $10,000, consider hiring a professional. Services like CoPatient or Solace Health specialize in auditing bills for a percentage of the savings they find. These advocates speak the language of billers and can often spot technicalities that a layperson would miss, such as "upcoding" or illegal balance billing.

Resolution Case Studies

Case 1: A patient in Texas received a $64,000 bill for an emergency ER visit involving a heart rhythm issue. By requesting the itemized bill, they found a $12,000 charge for a room they were never admitted to. After pointing out this "clerical error" and citing Fair Health Consumer data, the hospital settled for $8,000.

Case 2: A family was billed $18,000 for a birth after their insurance denied the claim due to a missing "prior authorization." The family used a medical advocate from Patient Advocacy Foundation. The advocate proved the birth was an emergency, making prior authorization unnecessary under the plan's own rules. The bill was reprocessed, leaving the family with only their $2,000 deductible.

Strategic Checklist

| Phase | Action Item | Outcome |

|---|---|---|

| Immediate | Request Itemized Bill + CPT Codes | Identifies ghost charges. |

| Audit | Cross-check codes on Fair Health | Sets Fair Market Value. |

| Eligibility | Apply for Hospital Charity Care | Potential 100% debt waiver. |

| Legal | Verify No Surprises Act | Cuts out-of-network fees. |

Avoiding Financial Errors

Do not assume your insurance company is fighting for you. They often process claims via automated systems that don't flag overcharges. You must be your own auditor. Also, never give your credit card info to a hospital "on file" during check-in; this allows them to charge balances without your prior review of the itemized statement.

Another error is waiting too long to act. Once a bill is sold to a third-party debt collector, your leverage decreases significantly. Start the dispute process within 30 days of the first statement. If a collector calls, immediately send a "Debt Validation Letter" via certified mail, which legally requires them to prove the debt is accurate before they can contact you again.

FAQ

Will disputing a bill hurt my credit?

No, the act of disputing does not hurt your credit. Furthermore, the three major credit bureaus (Equifax, Experian, TransUnion) do not report medical debt until it is at least one year past due, and they no longer report medical debts under $500.

What if the hospital refuses to negotiate?

If a billing department is rigid, escalate to the "Patient Advocate" or "Ombudsman" office at the hospital. These departments are designed to resolve disputes and have more authority to grant discounts than the standard billing clerks.

Can I negotiate even if I have insurance?

Yes. You can negotiate your "patient responsibility" portion. If you have a $5,000 deductible you can't afford, the hospital may still apply charity care or a prompt-pay discount to that specific amount.

How do I find a CPT code?

The CPT code is a five-digit number found on your itemized bill. You can look these up on the American Medical Association website or use a search engine to find the specific procedure name associated with the code.

Is a payment plan better than a settlement?

A lump-sum settlement is usually better because hospitals are often willing to take 50% of the total if paid immediately. Only use a payment plan if you cannot afford a settled lump sum, ensuring it is at 0% interest.

Author's Insight

In my years of navigating the healthcare finance landscape, I have found that the biggest hurdle is emotional, not financial. People feel guilty or ashamed of medical debt, which keeps them from negotiating aggressively. Remember that medical billing is a business transaction, and the "price" is often just a starting suggestion. I once helped a colleague reduce a $12,000 bill to $1,500 simply by highlighting that the hospital had "upcoded" a level 3 ER visit to a level 5. Always stay calm, document every phone call name and date, and never accept the first offer.

Summary

Managing a massive medical bill requires a shift from a passive patient to an active auditor. Start by securing an itemized statement, identifying errors through CPT code research, and applying for hospital financial assistance programs. By leveraging federal protections like the No Surprises Act and utilizing market-rate data to negotiate, you can significantly lower your financial burden. Take immediate action to keep the debt out of collections and protect your long-term financial health.